Q3 Investment Outlook

This data captures behavioral trends across tens of thousands of portfolios and is estimated to capture just over 10% of outstanding fixed income securities globally.

Q3 2024

After a first quarter characterized by consistently hotter-than-expected data prints, US data became more of a mixed bag in Q2. But more in-line inflation prints alongside signs of softness emerging in consumer activity don’t appear to have bolstered confidence in imminent rate cuts by the Federal Reserve (Fed).

Rather, the mixed set of data seems to have exacerbated uncertainty around the timing and depth of the Fed’s cutting cycle. And the added challenge of the US presidential election continues to weigh on institutional demand for US debt.

Aggregate US Treasury inflows have ebbed toward neutral alongside a dramatic drop-off in corporate debt flows (Figure 1). This moderation in US debt demand was initially accompanied by a surge in emerging market (EM) sovereign demand toward the end of May, with aggregate EM sovereign bond inflows reaching their highest level since February 2018 as the month drew to a close.

Inflows have since moderated, suggesting overall EM and developed market (DM) debt demand are now in a similar place. Elsewhere, appetite for European sovereign debt appears mixed against a backdrop of ongoing political uncertainty and several central banks in the early innings of their cutting cycles.

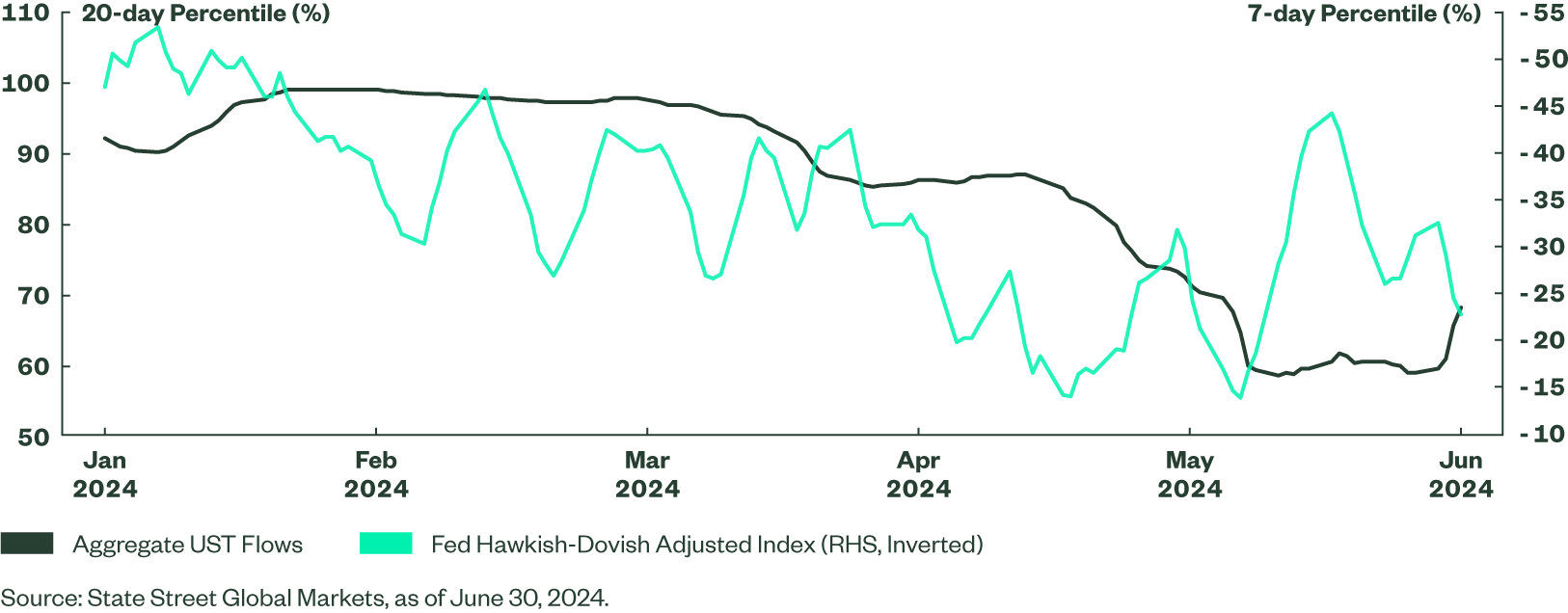

US Treasury Inflows Ebb

Institutional investors’ demand for US Treasurys waned throughout the quarter, as reflected by 20-day aggregate US Treasury (UST) inflows moderating to the 68th percentile. Inflows drifting down to their lowest level since a Treasury sell-off spurred by regional banking collapses in the spring of 2023 is notable given that they had remained above the 90th percentile for much of the past year. In fact, aggregate UST inflows printed in the 94th percentile as recently as the end of the first quarter. During this time, robustness reflected in growth and inflation data did little to quell investor conviction that cuts were forthcoming as Fed messaging was interpreted as extremely dovish. It appears UST demand fell in Q2 only as the Fed’s tone grew increasingly less dovish throughout the quarter (Figure 2).

Looking under the hood at sovereign bond flows by key maturity, this pullback in increasing exposure to USTs was consistent across 2-, 5-, and 10-yr USTs. But the move down has been most pronounced in 10-yr UST inflows, which have fallen dramatically to the 13th percentile from the 97th at the start of Q2. In a similar vein, aggregate US corporate bond inflows are currently in the 33rd percentile, a steep decline from the 98th as investor confidence in corporate resilience continues to diminish the longer policy remains restrictive.

Figure 2: Dovish Fed Driving Treasury Demand

Demand for Inflation Protection Diverges

Institutional demand for inflation protection surged at the start of the quarter on the back of an upside surprise to March’s CPI print. Since then, aggregate inflows to US Treasury Inflation-Protected Securities (TIPS) have eased back to the 35th percentile alongside in-line to slightly weaker-than-expected April and May price prints.

A breakdown of TIPS’ inflows by key maturity reveals that demand for inflation protection has dropped off the most sharply for a two-year time horizon (Figure 3); 2-yr US TIPS inflows have fallen to the 19th percentile from as high as the 98th in April. Meanwhile, 5-yr US TIPS inflows have risen to the 62nd percentile from the 8th at the end of Q1. And inflows for 10-yr UST TIPS are not far behind, hovering around the 50th percentile. This divergence in demand for TIPS by maturity suggests a more sanguine short-term inflation outlook among institutions as activity begins to moderate while greater uncertainty emerges around demographic and debt sustainability issues that threaten to perpetuate upward price pressures in a 5- to 10-year time horizon.

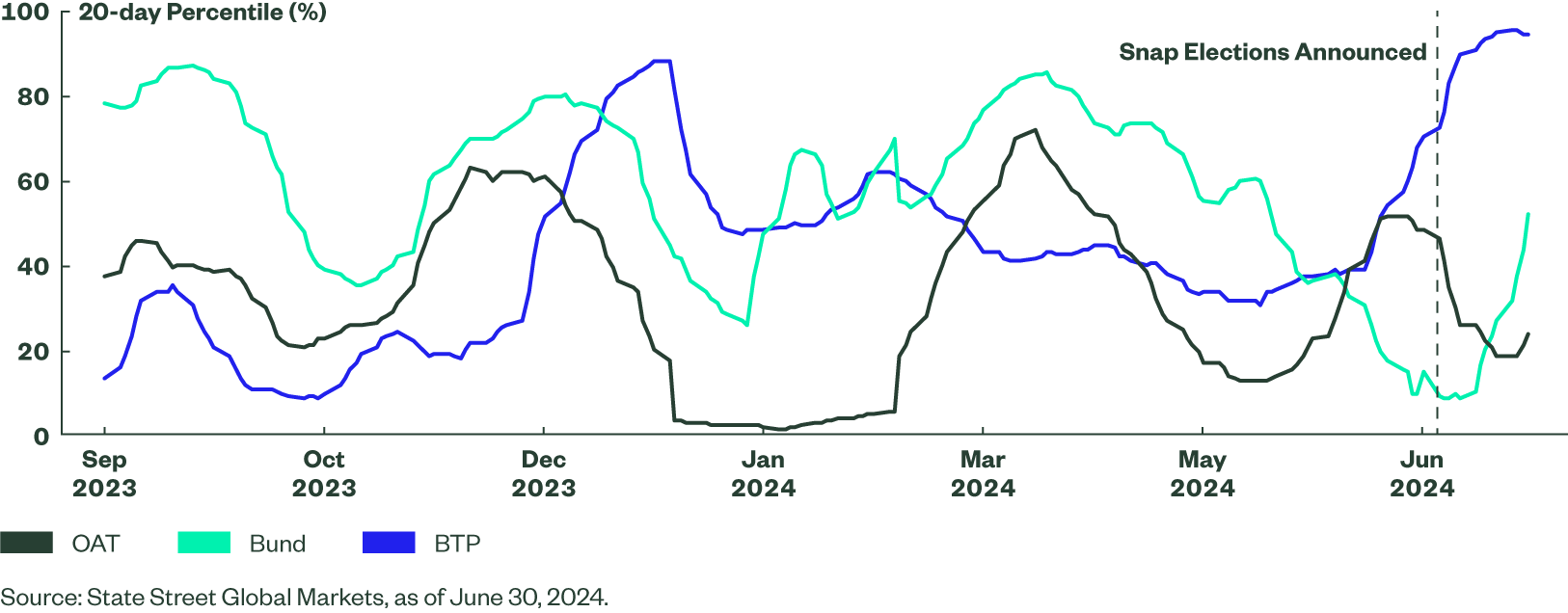

European Debt Appetite Amid Political Uncertainty

Elsewhere in the DM sovereign space, behavioral data revealed real money’s reaction to the political drama in Europe throughout the quarter. The 10-yr French OAT-German bund spread recently widened by almost 30 basis points (bps) on the back of uncertainty prompted by French President Macron’s call for snap parliamentary elections (Figure 4).

It appears, however, that a retreat in institutional demand for France’s debt upon the election announcement has been confined to the shorter end of the curve. Investors certainly exhibited some caution in becoming more selective in where they increased their exposure to European debt, as a moderation in 2-yr OAT inflows to the 24th percentile from the 64th at the start of Q2 coincided with an acceleration in 2-yr bund and continued BTP buying. A steady increase in 10-yr OAT flows throughout the quarter, however, suggests there is little longer-term concern about France’s fiscal risks currently being factored into real money decision-making. Inflows to 10-yr BTPs saw a similar pick-up over the past few months, while demand for 10-yr bunds dropped off notably.

Figure 4: Institutions Exhibit Caution in 2-yr EGB Inflows