The Case for Defensive Equity Strategies

From a risk-adjusted return point of view, the merits of low volatility and defensive strategies remain compelling. In this article, we look at how - despite the challenging market setup for defensive strategies – these approaches have broadly achieved better Sharpe ratios and how our active defensive strategy can help provide a balance of risk mitigation and potential market upside.

Since January 2009, the defensive and low volatility themes have lagged the market. The MSCI World Minimum Volatility Index underperformed the MSCI World Index by 1.4% per annum over the period from January 2009 to the end of March 2024. However, focusing purely on returns overlooks a critical aspect of low-volatility and defensive strategies. While the quest for lower risk has exerted a significant cost to relative performance over the past decade and a half, from a risk-adjusted return point of view, the merits of these strategies remain compelling. Defensive and low-volatility indices have broadly achieved better Sharpe ratios than the market over the period. (See Figure 1.) Our active defensive strategy, which incorporates both defensive portfolio construction as well as active stock selection, has done even better – with a risk-adjusted outcome since inception that significantly improved upon the investment results of both market and passive low-risk indices.

Figure 1: Risk And Returns Outcome (January 2009 – March 2024)

| MCI World | MCI World Minimum Vol | Global Defense Equity | |

|---|---|---|---|

| Ann. Retuns | 11.14 | 9.21 | 10.47 |

| Ann. Volatility | 15.60 | 11.12 | 11.51 |

| Sharpe Ratio | 0.65 | 0.74 | 0,83 |

Source: MSCI, SSGA. As of March 2024. Index returns reflect capital gains and losses, income, and the reinvestment of dividends. Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Past performance is not a guarantee of future results.

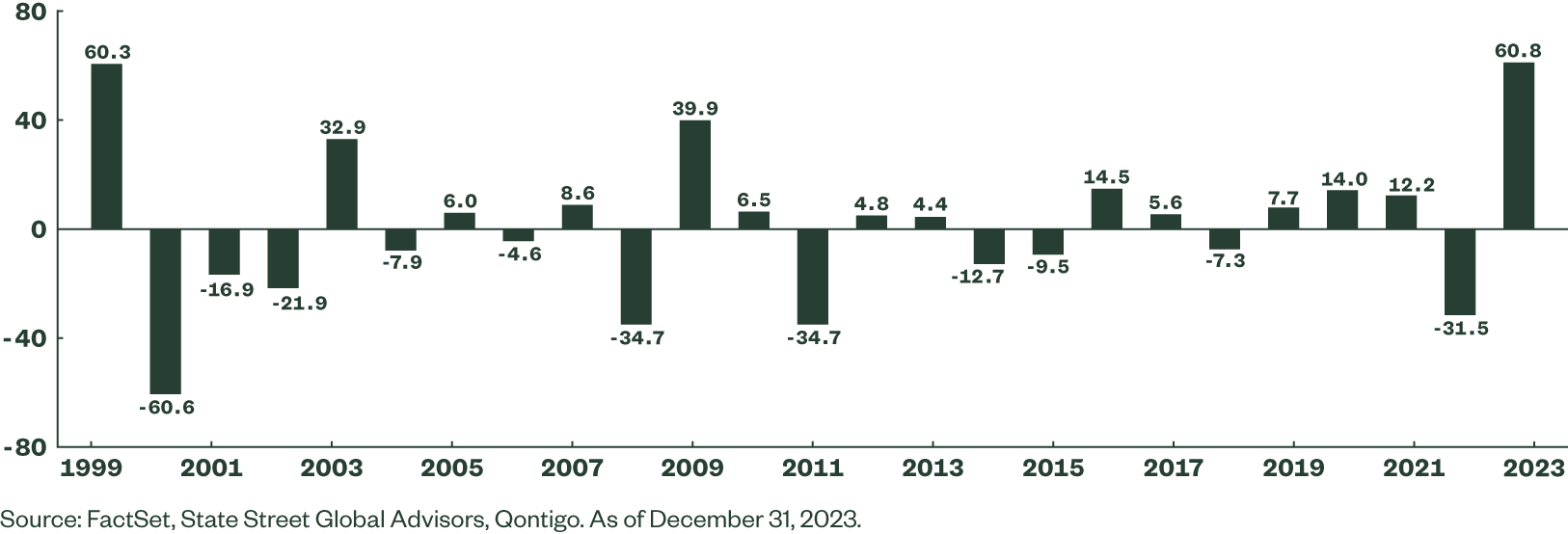

These improvements in investment outcomes were achieved despite the challenging market setup for defensive strategies in the post- Global Financial Crisis era. The pandemic factor injected even further headwinds for the performance of low-volatility strategies. Specifically, the ultra-low interest rate policies of global central banks kept risk appetite elevated for most of the period following the Global Financial Crisis, creating a rather ebullient equities market backdrop of persistently strong returns punctuated by very few and shallow market drawdowns. A little more than a decade later, an overwhelming fiscal pandemic response in excess of $5 trillion (in the US alone) breathed new life into several risk trades. Finally, the AI boom came just in time to re-energize the high-growth, higher-risk trades when they were running of steam in 2022. Investors’ rush for high-risk, high-growth stocks reached a feverish pace in 2023, culminating with a 60% outperformance of highest beta quintile portfolio vs. lowest beta quintile portfolio. (See Figure 2.) In our view, the tide is potentially changing. We may be entering a market environment that would be more favorable for defensive strategies. Investors should keep defensive strategies in their arsenal of investment options to navigate a potentially changing investment climate ahead.

Figure 2: Performance Spreads Between Highest and Lowest Beta Quintile

Based on long-term historical analysis, the strong pendulum swing for high-risk/high-growth companies that we witnessed in 2023 is unsustainable. As shown in Figure 2, the period following a large high-beta payoff tends to be followed by the pendulum swinging to the other side or, at best, an extended period of more moderate payoffs. To the extent that the extremely positive payoff to high-beta tends to be associated with a sharp market rally, the moderation of beta payoffs tends to occur in a market environment where the base of the market rally either reversed or broadened. So far this year, we had seen a broadening of the market rally, with low-beta equities catching up on market upside.

Beyond the recent improvement in low-beta equity performance, we believe there are a myriad of other market factors that could further reduce the headwinds for low-beta equity over the near future. First, the ideal conditions that have kept market volatility low over the past decade and a half are fading. The ultra-loose central bank policies that have tipped the scales in favor of higher risk are tightening which in our view means that higher-beta stocks are unlikely to produce the returns that they have in the past.

The inflation impulse of the economy likely remains elevated, given the tight labor markets and aging populations in developed countries. Furthermore, the disinflationary forces from China are now under pressure as trade tensions with the West escalate. On the fiscal side, the post-pandemic fiscal stimulus has left most developed countries saddled with large deficits and a high level of public sector debts, potentially limiting the type of overwhelming force of bailouts and Quantitative Easing phases that helped limit market collapses since 2008.

Those looking for relief from the geopolitical realm are likely to be disappointed. The escalating conflict between Ukraine and Russia is showing few signs of resolution. Meanwhile, the Middle East is serving up new conflicts that could destabilize the energy markets. In our view, one casualty of the adjustment process is rather obvious – the low-volatility, stable market that marked the last two decades is going away. However, our base case assumption is for volatility to be moving higher – much higher. As market volatility drifts higher, the merits of being defensive would naturally accrue over time with larger swings of the market.

Obviously, not all is gloom and doom for the market. We are aware of the large reservoir of cash sitting on the sideline that could potentially mitigate any emerging bout of market downside. Further, all indications are that we are heading into a period of significant technological disruption driven by recent breakthroughs in AI technology. These periods of significant technological advances create new sets of winners and losers. The same market forces that have impeded the returns of defensive exposures may prove enduring. Furthermore, pure low-volatility exposures may entail loading up on high levels of unintended macro exposures, such as interest rates sensitivities. That’s why, in our view, active defensive strategies should steer away from the potential pitfalls of value traps and excessive exposure to interest rates risk. Active strategies offer more diversified sources of returns that may be better suited to navigate uncertain investment environments.

In fact, the recent performance of our active strategies lends credence to this narrative. With the normalization of real interest rates, active stock selection alpha has vastly improved over the past few years. As shown in Figure 2, the extremely strong low-beta headwind in 2023 proved impossible to overcome and we underperformed the market – despite positive value added from stock selection. However, our active strategy performance was significantly better than the MSCI Minimum Volatility Index. As low-beta headwinds dissipated so far this year, positive stock selection performance has delivered positive active performance versus the market, despite a continuation of strong market performance. (See Figure 3.)

Figure 3: Improvement in Stock Selection Model Performance

| Returns | MSCI World | MSCI World Minimum Vol | Global Defensive Equity |

|---|---|---|---|

| Year 2023 | 23.79 | 7.42 | 7.31 |

| YTD 2024 | 8.88 | 5.63 | 9.72 |

Source: MSCI, State Street Global Advisors. As of March 2024. Index returns reflect capital gains and losses, income, and the reinvestment of dividends. Past performance is not a guarantee of future results.

The Bottom Line

We expect heightened market uncertainty ahead as the confluence of geopolitical, demographic, and policy risk intersects with the disruptive forces of AI and technology innovations. In our view, our active defensive strategy provides the proper balance between risk mitigation and participation in potential further upside in the market. It should remain a key consideration among the arsenal of investment solutions available for investors to navigate the challenging investment landscape ahead.